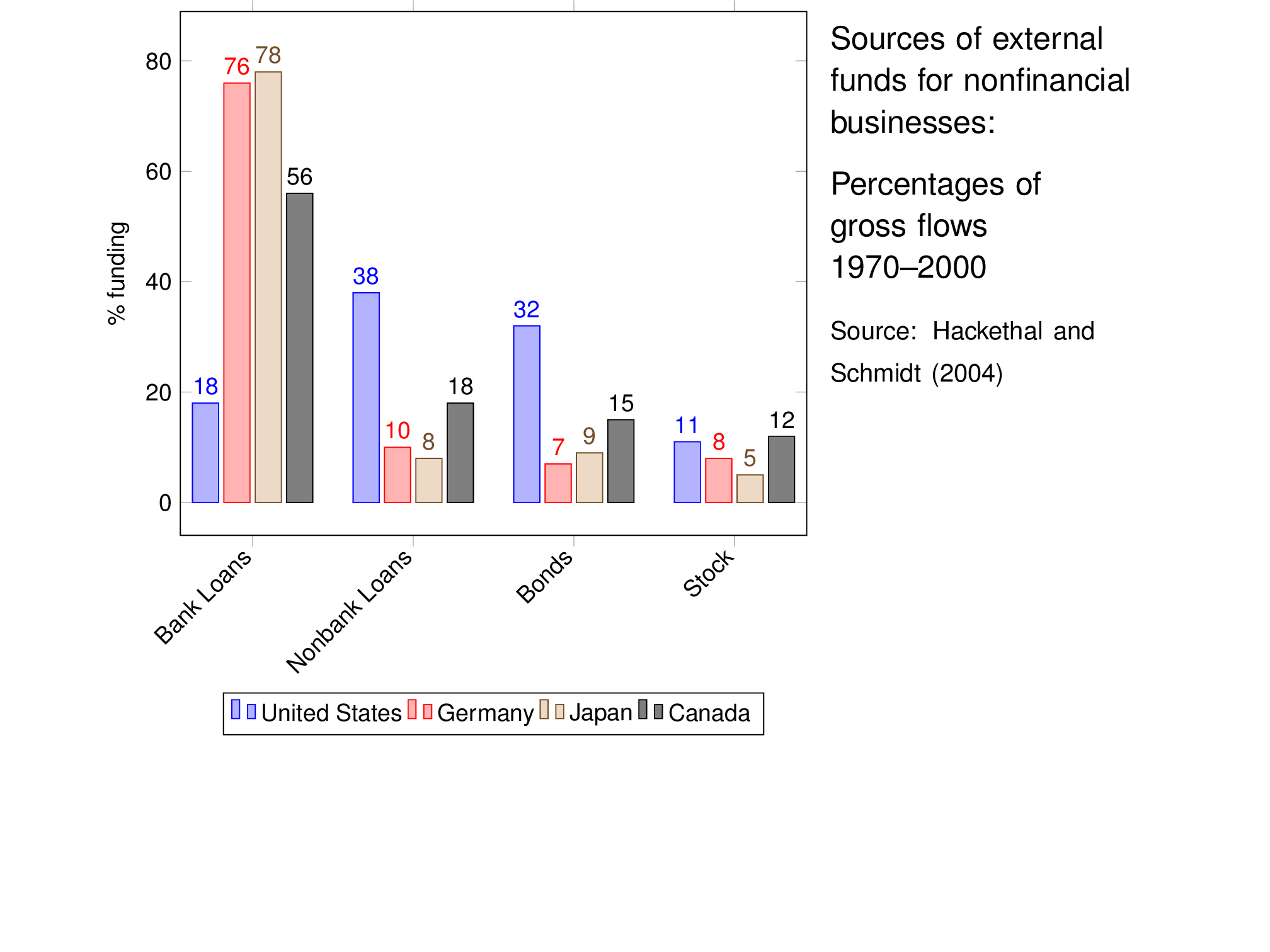

class: center, middle, inverse, title-slide # DSBA 20598 – FinTech and Blockchains ## Lecture 2: Financial Intermediation ### Prof. Silvio Petriconi ### Department of Finance, Bocconi University ### 2019-09-12 (updated: 2019-09-18) --- class: finance-slide, inverse, left #Financial Intermediation -- ### | Asymmetric information and adverse selection ### | Banks as informed lenders ### | Liquidity transformation --- .left-column[ ##Our goal today] .right-column[Since we're interested in technologies that can have disruptive effect on banking, we'll spend today's class learning about various facets of financial intermediation. Most of external funds of non-financial firms come from financial intermediaries, not from markets. That is at first glance surprising: what's the economic function of the intermediary? I'll put on my economist hat today to give you the details. We'll learn about the consequences of asymmetric information, and why intermediaries are able to overcome barriers to trade in this setting. We'll also learn why intermediaries are potentially fragile. ] --- class:top, left # Banks provide most external funding - why?  --- class:inverse,center,middle background-image:url("img/bubble-gum-438404_1920.jpg") background-size:cover background-position:center #Adverse selection --- #Introduction __Asymmetric information__ is one of the most important concepts in financial economics: - it arises whenever in a transaction one side has more (relevant) information than the other side - it comes in two “flavors”: * __Adverse selection:__ *before* agreeing on some transaction, one of the two parties has some relevant information that is not known to the other party * __Moral hazard:__ *after* agreeing on some transaction, one party can take an action to its own benefit that is not observed by the other party --- #Adverse selection - Imagine there is a transaction to be made: a health insurance is about to win a client; a lender is about to make a loan; somebody is about to buy a used car. - In each of these examples, there is one side that is better informed than the other: - the health insurance may not know how bad a risk the customer is (whilst the customer knows) - the lender may not know how reliable the borrower really is (whilst the borrower knows) - the buyer of the car may not know whether it has hidden defects (whilst the seller knows) - In such situations, markets don’t function very well: --- #The curse of adverse selection In our examples, - the insurance will ask for a relatively high premium (because the most risky patients will be most keen on getting insurance) - the lender may ask for a relatively high interest rate - the buyer of the car may only be willing to buy at a steep discount in price (reflecting the *average* quality of cars on the market) But then the best types, - the healthiest clients seeking insurance, - the safest borrowers asking for a loan, - the sellers of excellent used cars may withdraw from the market because they can no longer attain reasonable conditions for the transaction. --- #Overcoming adverse selection We call this *adverse selection* (because good types may withdraw whereas poor types are more likely to stay in the market). It makes it very hard or impossible to trade an asset on which one side has more information than another `\(\Rightarrow\)` _illiquidity_. __Countermeasures:__ What can be done against adverse selection? Answer: _Reduce / eliminate information asymmetries!_ - government regulation to increase information - private collection of information - example: health examination before taking insurance - but in the context of securities purchases, there can be free-rider problems: if you generate private information and act based on it, others may observe your actions, imitate them and free-ride - in the context of securities, one can solve the free-rider problem if, after acquiring information, the security is purchased exclusively by an informed intermediary: bank lending! --- class:center,inverse,middle background-image:url("img/dollar-2891817_1920.jpg") background-size:cover background-position:center #Banks as informed lenders --- # Informed lending There is broad consensus in the banking literature that one key activity of banks is __information acquisition__: * They acquire information ex-ante (before the loan is approved) to know more about their borrowers and mitigate adverse selection. * They keep collecting further information ex-post (after the loan has been made) to ensure that the money is not used for improper purposes (we call this _monitoring_). For example, most banks that lend to construction firms have their own construction engineers that regularly visit the construction site and evaluate progress before the next tranche of the loan is paid out. --- # Relationship banking If banks keep acquiring information over the entire course of a credit agreement, they end up being better informed about the borrower than anyone else when the loan has been repaid: banks learn by lending. It is therefore quite natural that many banks, especially small ones with dense branch networks, invest in building long-lasting relationships with their borrowers. For borrowers, this is double edged sword: better informed relationship lenders offer more reliable access to credit, but can also afford charging higher interest because they enjoy an information monopoly over their long-term borrower.* .footnote[*The idea of hold-up in a borrowing relationship was first presented by [Sharpe, 1990](https://doi.org/10.1111/j.1540-6261.1990.tb02427.x).] --- # Relationship banking: geographic proximity Most relationship lenders are in close geographic proximity to their borrowers and have a dense branch network. For example, [Degryse and Ongena](https://doi.org/10.1111/j.1540-6261.2005.00729.x) (2005) find in a study of Belgian banks that banks are geographically close to customers: The median borrower is located around 4 minutes and 20 seconds from the lender at a travel speed of 20 mph, i.e. 2.25 km distance. There's plenty of evidence that the quality of a bank's information for the purposes of lending deteriorates substatially with increasing distance to its borrowers, see e.g. [Granja, Leuz and Rajan](https://www.ssrn.com/abstract=3271079) (2018). In other words, credit-relevant information is to a substantial share of _local_ nature. --- # Informed lending in a digital world These days, Facebook, Google and other techs know much more about us than all banks combined. Banks' information advantage has eroded. This creates new opportunities for entry. Moreover, we all leave digital data traces every single day. FinTech lenders have been using people's [digital footprint](http://money.cnn.com/2013/08/26/technology/social/facebook-credit-score/) in facebook and other social media for quite some time to evaluate the creditworthiness of applicants who have no official credit score. Are such data any good? It seems so: [Berg, Burg, Gombovi and Puri](https://www.nber.org/papers/w24551.pdf) (2018) have shown in a dataset of 250,000 registrations at a German e-commerce website that the digital traces that we are leaving while shopping online are more precise predictors of our creditworthiness than the credit scores of credit bureaus. We will talk much more about alternative creditworthiness testing in the second half of the course. --- class:center,inverse,middle background-image:url("img/drop-3065629_1920.jpg") background-position:center background-size:cover #Liquidity transformation --- #Illiquid bank assets In acquiring information, banks reduce the information gap between lenders and borrowers. This has another side effect: the better the bank knows its borrowers, the greater becomes the bank's information advantage over anyone else in the economy as far as its loans are concerned. This is no problem if the bank never has to sell any loans. But it also means that the loans will be very illiquid and hard to sell because the bank's information advantage creates asymmetric information problems between the bank and the prospective buyers of the loans. As many loans have long maturities whilst most bank deposits can be withdrawn anytime, this is a potential problem. We'll demonstrate the consequences of this __liquidity transformation__ in the [Diamond-Dybvig (1983)](https://www.jstor.org/stable/pdf/1837095.pdf) model. .footnote[*The notation follows Ch 2.2 of [Freixas and Rochet's "Microeconomics of Banking"](https://mitpress.mit.edu/books/microeconomics-banking-second-edition)] --- # Diamond-Dybvig (1983) ### An illiquid asset Let's model an illiquid asset in a stylized way: * There are three periods `\(t=0, 1, 2\)`. * The illiquid "long" asset matures in period `\(t=2\)`. * Every unit of the long asset gives `\(t=2\)` a payoff of `\(R>1\)`. If liquidated early in `\(t=1\)`, however, it can only be sold at a value `\(l < 1\)`. ### Consumers There is a continuum of identical consumers. Each has an endowment of 1 at `\(t=0\)`, and can consume at either `\(t=1\)` or `\(t=2\)`. At the beginning of the game in `\(t=0\)`, consumers don't know (yet) when they will want to consume. --- ### Liquidity preferences At `\(t=0\)`, consumers are not certain as to when they want to consume. They will learn about this only in `\(t=1\)`. There is a probability `\(\pi_1\)` that they need to consume early in `\(t=1\)`. We will call those early consumers the _impatient_ consumer types. With probability `\(\pi_2=1-\pi_1\)` they are _patient_ and consume late in `\(t=2\)`. Assuming a concave utility function `\(u(\cdot)\)` with `\(u^\prime > 0, u^{\prime\prime} < 0\)`, their utility from consuming `\(c_1\)` in period 1 and `\(c_2\)` in period 2 is therefore given by $$ u(c_1, c_2) = \left\lbrace \begin{array}{ll} u(c_1) & \text{w. prob.}\pi_1 \newline u(c_2) & \text{w. prob.}\pi_2 \end{array} \right. $$ This model assumption captures what one can observe as a pervasive pattern in financial markets: investors are hesitant to purchase illiquid financial assets because they don't know when they will need the money due to an unforeseen liquidity shock. --- ## Solving the model ### Benchmark 1: Autarky. If consumers are unable to trade with anyone, what would their allocation be? How much welfare would they enjoy? If they invest in `\(t=0\)` an amount of `\(I\)` in the long asset and `\(1-I\)` in the short asset, then: * If they end up being impatient, they get to consume `\(c_1=lI+(1-I)\)` by liquidating the long asset early in `\(t=1\)` plus consuming all short asset payoffs. * If consumers end up being patient, they obtain `\(c_2 = RI + (1-I)\)` in period `\(t=2\)`. How much can they consume if they choose `\(I\)` optimally? Without solving this question, we can see that because of `\(l<1\)`, any choice of `\(I\)` implies that `\(c_1 \leq 1\)` and `\(c_2 \leq R\)`, with __one of these two inequalities holding strictly.__ It is not possible to attain a consumption of `\(c_1=1, c_2=R\)` in autarky. --- ### Allowing for trade If we allow consumers to trade between each other, we can improve upon autarky. This would work by allowing impatient consumers to sell in `\(t=1\)` a bond to patient consumers: instead of liquidating the long asset at a loss, they would keep holding it, sell a bond in `\(t=1\)` to patient consumers that offers one unit of consumption in `\(t=2\)` for price `\(p\)` in `\(t=1\)`, use the proceeds from selling the bond to consume early, and repay the bond with the payoff of the long asset in `\(t=2\)`. Patient consumers would use all their short asset holdings to purchase `\((1-I)/p\)` bonds in `\(t=1\)` from impatient consumers. $$ c_1 = pRI + (1-I) $$ $$ c_2 = RI + \frac{1-I}{p} $$ As you can see, the two equations imply that `\(c_1 = p c_2\)`. Note that the utility of agents increases in `\(I\)` if `\(pR > 1\)`, and decreases in `\(I\)` if `\(pR < 1\)`. This means that the only price at which an interior optimum `\(I\in(0,1)\)` can exist must satisfy `\(pR=1\)`, hence `\(p=1/R\)`. --- ###Allowing for trade (cont.) What are the allocations that are attained? Plug `\(p=1/R\)`, and for any `\(I\)` we get `\(c_1 = 1\)`, and `\(c_2 = R\)` which is strictly better than autarky. ###Benchmark 2: Can one do even better? Let's ask a benevolent social planner to allocate resources at will as to maximize expected utility of all agents in the economy. It will surely be optimal to pay for all `\(t=1\)` consumption with the short asset, and for `\(t=2\)` consumption with the long asset. The optimization problem becomes `$$\max_{c_1, c_2, I} \pi_1 u(c_1) + \pi_2 u(c_2)$$` subject to `$$\pi_1 c_1 = 1-I \text{, and}\\ \pi_2 c_2 = RI$$` --- Substituting the constraints into the objective function, we have $$ U(I) = \pi_1 u\left(\frac{1-I}{\pi_1}\right) + \pi_2 u\left(\frac{RI}{\pi_2}\right) $$ which we can maximize by differentiating with respect to `\(I\)`. This yields the first-order condition $$ -u^\prime(c_1^\ast) - Ru^\prime(c_2^\ast) = 0 $$ Our solution with trade, `\(c_1 = 1, c_2=R\)` will satisfy this condition at best by coincidence: __The market solution is not efficient here.__ In particular, if `\(u^\prime(1) > Ru^\prime(R)\)`, there is more marginal benefit to first period consumption than what the (incomplete) market solution attains: `\(c_1^\ast > 1\)`. ### Banks A financial intermediary could receive deposits of `\(1\)` at `\(t=0\)` and promise withdrawal of `\((c_1^\ast, c_2^\ast)\)` in `\(t=1\)` and `\(t=2\)`, respectively. By law of large numbers, the aggregate impatient and patient consumers withdrawals are deterministic, and by choosing `\(I\)` accordingly, the planner's optimum can be reproduced including `\(c_1^\ast>1\)` which benefits impatient consumers. --- ### Liquidity intermediation and financial panics What banks essentially are in the Diamond-Dybvig model is __liquidity intermediaries__: they hold illiquid assets, yet they allow withdrawal of liquid deposits at any point in time, providing liquidity insurance for depositors. This is a great benefit. We think it's one of the core functions of banks. But the same liquidity transformation is also the root of inherent __instability__: the bank can only meet the withdrawals of the impatient depositors from short asset liquidations. Imagine that some patient depositors come to believe that other patient depositors are withdrawing `\(c_1 > 1\)` in `\(t=1\)`. Then they must conclude that the bank must liquidate the long asset at a loss to meet those withdrawals, and not enough is left to pay them `\(c_2^\ast\)`; if they believe that enough other patient depositors are withdrawing early to make their payoff fall below `\(c_1^\ast\)`, they will want to withdraw immediately. The result is a __bank run__: both patient and impatient depositors attempt to withdraw at `\(t=1\)`. Beliefs about others withdrawing early suffice to sustain a financial panic. --- #Deposit insurance and moral hazard This key insight of Diamond and Dybvig (which was refined later by [Goldstein and Pauzner, 2005](https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1540-6261.2005.00762.x)) is that liquidity transformation makes banking inherently unstable and runs can occur because of depositors' beliefs about other depositors' actions. The problem of depositor runs is not limited to traditional financial intermediaries. Every liquidity transformation opens up the potential for runs. One way of resolving depositor runs is government-provided _deposit insurance_: if an insurance guarantees that all depositors will always receive their promised payment, patient consumers will no longer run. This can create stability, but it's a double-edged sword: deposit insurance also induces banks to take greater risks into their books because deposits rates will becomes less sensitive to the actual risk that the bank is exposed to. After all, due to insurance, depositors are always paid! For this reason, depository institutions are subject to heavy oversight by regulators to discourage such _risk shifting_. --- class: center, middle, inverse #Discussion --- class: center, middle # Thanks! More material on [https://silviopetriconi.github.io](https://silviopetriconi.github.io). For questions, comments and suggestions regarding these slides please contact the author, [`silvio.petriconi@unibocconi.it`](mailto:silvio.petriconi@unibocconi.it). <br></br> [](http://creativecommons.org/licenses/by-nc-sa/4.0/) <br></br> This work is licensed under a [Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License](http://creativecommons.org/licenses/by-nc-sa/4.0/).